Repo markets play one of the most important roles in the financial systems. Unfortunately, most investors don’t have a clear idea about it. If you are one of them, this article is for you. We will help you to get a better understanding of what repo markets are all about and navigate through the basics. You can also learn more about the history of the repo markets and how they evolved.

What Are Repo Markets?

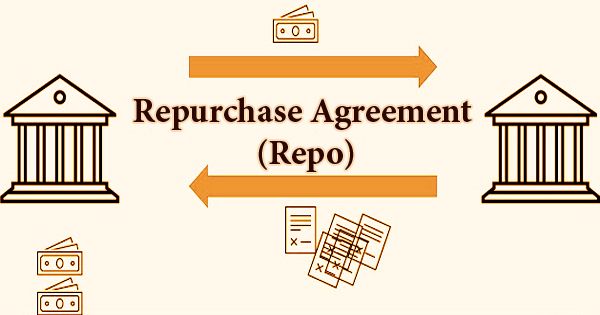

A repo (repurchase agreement) is a short-term collateralized loan much like a secured, short-term cash loan. In a repo transaction, the borrower sells certain securities to a lender and agrees to buy them back at a slightly higher price after a short period. This short period can be as little as overnight.

For the party selling the security and agreeing to repurchase it in the future, it is a repo. For the party on the other end of the transaction, buying the security and agreeing to sell in the future, it is a reverse repurchase agreement or reverse repo.

In practical terms, repos allow institutions that own lots of securities to obtain cash quickly while other institutions with lots of cash can earn extra income with very low risk. Repo markets connect security owners who want cash with cash owners who want low-risk collateral. The short-term nature makes them attractive as a source of liquidity.

Why Repo Markets Matter

Repo markets matter for two critical reasons. First, they are crucial for bank funding. Banks regularly borrow and lend money in the repo market to fund their day-to-day operations. Being able to readily obtain cash and liquidity is vital for their business.

Second, repo markets provide an avenue for central banks to support financial markets during periods of stress. Central banks enact monetary policy and ensure adequate liquidity partly through the repo market. This was critical during the 2007-2009 crisis.

How Repo Markets Work

There are two main parties in repo agreement transactions – the cash borrower who offers securities as collateral and the cash lender who accepts them. Here is the sequence:

- The borrower sells certain securities to the lender at an agreed initial price. This gives the borrower the cash they want.

- The parties agree to reverse the transaction at a future date, with the repurchase price slightly higher than the original sale price. The difference between the sale and repurchase price represents the interest rate on the cash loan.

- When the term of the repo ends, the transaction unwinds. The borrower buys back the securities they initially sold at the higher repurchase price. That returns the securities to them, while repaying the loan plus interest to the lender.

Then the process can repeat, allowing the cash borrower to maintain liquidity as needed.

Types of Repo Markets

There are three primary segments of repo markets:

- Tri-party repo market – A third-party clearing bank manages the transaction to reduce risk. This is the biggest segment in the US and one of the safest.

- Bilateral repo market – The two principals in the transaction deal directly with each without third-party clearing. Some risk still remains.

- Inter-dealer repo market – These transactions occur between the large securities dealers and banks to raise short-term capital.

What Are the Risks?

Repo markets facilitate the flow of liquidity through the financial system. However, like everything in finance, they also come with risks such as:

Counterparty risk – One party in the repo transaction may default before settlement. Collateral risk – The assets used as collateral may fall in value during the repo term.

Rollover risk – Borrowers may struggle to obtain cash for new repos to repay maturing ones. Haircut risk – Parties may demand greater discounts or haircuts to the value of collateral.

If not managed properly at a systemic level, these risks can trigger liquidity crises.

The 2007-2009 Financial Crisis

The 2007-2009 Global Financial Crisis underscored the significance and weaknesses of the repo system. Repo markets were a key mechanism propagating and accelerating liquidity problems among banks.

Precisely, here is how repo markets exacerbated the crisis:

- Banks became extremely reliant on short-term repo funding markets, exposing them to maturity mismatches and rollover risk.

- Collateral value fell, forcing haircuts and margin calls that put weaker banks into liquidity traps.

- Counterparty risk created uncertainty given poor transparency about bank exposures.

- Interbank lending stalled due to panic over counterparty solvency, choking liquidity flows.

Once the crisis hit, the US Federal Reserve was forced to intervene aggressively via liquidity injections to support struggling banks and keep the repo system functioning. The crisis accentuated systemic issues of opacity, interconnection and maturity mismatch risks that policymakers continue working to address.

The Future of Repo Markets

Repo markets are likely to continue evolving in the coming years. Regulators may impose new rules and reporting requirements to improve transparency and reduce systemic risks. There will likely be a push towards developing centralized clearing and settlement infrastructure for repo transactions. This could help reduce counterparty risks and improve stability.

New technologies like distributed ledgers and smart contracts may also find applications in repo markets. These could enable automation of processes and help achieve quicker, more efficient repo transactions. However, adoption faces challenges around standardization and interoperability.

The repo market size will likely keep expanding as demand for short-term funding continues rising globally. The types of collateral used may also expand beyond just government securities to include other assets like equities, corporate bonds etc. Participation from non-bank entities like hedge funds, pension funds, insurance companies will likely rise too.

Overall, efforts by regulators and market participants will shape how repo markets progress. The goals would be to maintain stability, efficiency, transparency and adaptability to new technologies/participants. Recent volatility has underscored the need for proactive reforms.

Final Words

Repo markets support liquidity and cash flow through the global financial system daily. However, as seen in the 2007-2009 crisis, they can also rapidly propagate risks during periods of financial stress. It is important to keep this in mind and go ahead with your investments in the repo market.